The most common barrier among people who want to invest in Florida but haven’t yet is the down payment. Not the process, not the language, not the distance. The down payment.

That makes sense. For a $400,000 property with a foreign national loan, the minimum down payment is 25%, which equals $100,000. In the local currency of any Latin American country, that figure can seem unreachable. But there are investors from Colombia, Mexico, Peru, and Venezuela who reach that number faster than they expected because they have a concrete plan, not just an intention.

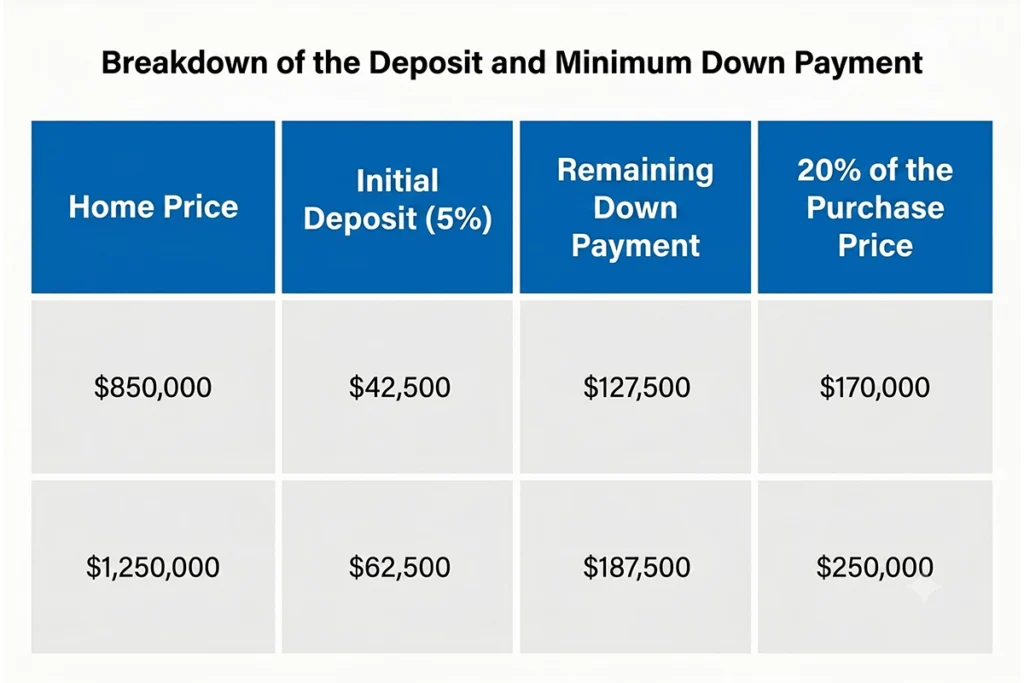

How much you actually need (beyond the 25%)

The most common mistake is calculating only the 25% and arriving at closing with exactly that. The down payment is the largest component, but not the only expense you need to cover.

Closing costs: Between 2% and 3% of the purchase price. For a $400,000 property, that’s between $8,000 and $12,000. They include lender fees, title insurance, recording fees, transfer tax (documentary stamp tax), and prepaid insurance and taxes.

Emergency reserve: Lenders for foreign nationals generally require proving you have between 3 and 6 months of mortgage payment in reserve after closing. For a $2,200/month payment, that’s between $6,600 and $13,200 that must be available in your account.

Furniture and equipment: If the property will operate as vacation rental, you need to fully furnish it before the first booking. For a 4–5 bedroom home in a resort community, the furnishing budget ranges between $15,000 and $30,000.

| Item | Estimated range ($400k property) |

|---|---|

| Down payment (25%) | $100,000 |

| Closing costs (2.5%) | $10,000 |

| Mortgage reserve (3 months) | $6,600 |

| Initial furnishing | $20,000 |

| Total to have available | ~$136,600 |

The real figure for a first investment in Florida is around $130,000–$150,000, not the $100,000 of the down payment alone. Plan based on the complete number.

Strategy 1: calculate your real savings speed

Before any strategy, you need to know at what speed you can save. Not what you want to save, but what genuinely remains after covering all your monthly expenses.

Take the last 6 months of your income and expenses. Calculate the average of what genuinely remained available for savings or investment. Multiply that number by 12. That’s your current annual savings rate, without any changes to your lifestyle.

If that number gives you $20,000 per year, you’ll reach $140,000 in 7 years. If it gives you $35,000 per year, you’ll get there in 4 years. If it gives you $50,000, in less than 3.

The point isn’t whether the number is large or small. It’s that you know it precisely so you can plan. Many investors overestimate what they can save and get frustrated. Others underestimate because they’ve never run the calculation and are surprised at how quickly they can get there.

Strategy 2: dollarize savings from day one

If you live in a country with currency devaluation (Argentina, Venezuela, Colombia, Peru), saving in local currency to buy in dollars is a race against time that you systematically lose.

The most important decision isn’t how much to save but in what currency to hold it. Every month your savings sit in pesos, soles, or bolivares while the dollar rises, you fall behind even while saving.

Options for dollarizing savings from Latin America:

Dollar accounts at local banks: Available in most countries. They protect against local devaluation but have low yields.

Accounts abroad: Uruguay and Panama are the most used destinations among Latin Americans for maintaining dollar accounts outside their countries. They’re accessible, have solid legal protection, and allow international transfers without complications.

ETFs and dollar-denominated funds: For savings you don’t need in the short term, investing in fixed income ETFs in dollars (American treasury bonds, for example) can generate a yield of 4%–5% annually while the money waits to be used for the down payment.

Stablecoins (USDC, USDT): For those in countries with severe exchange controls, stablecoins are a way to hold value in digital dollars. They have high liquidity and can be converted to real dollars when the time comes to transfer at closing.

Strategy 3: explore assets you already have

Many Latin American investors have the down payment partially accumulated in assets they don’t recognize as such.

Local property with equity: If you have a property in your country that has risen in value, you can refinance or sell it to free up capital. An apartment in Bogotá that you bought for $80,000 and is worth $150,000 today has $70,000 in equity that could become the down payment for a Florida property.

Investment portfolio: Stocks, investment funds, CDs, bonds. If you have an investment portfolio in your country, evaluating whether part of it should be reallocated to real estate in the U.S. is a valid strategic decision.

Partnership with family members or partners: Pooling capital between two or three people for the down payment is a common strategy. It requires a clear agreement on ownership, management, and exit strategy, but it divides the required amount. Two people contributing $70,000 each reach $140,000 faster than one person saves $140,000 alone.

Strategy 4: choose the right property to reduce the entry threshold

Not all Florida properties require the same down payment. The most effective way to shorten the time to your first investment may be to adjust expectations about the initial property type.

A $280,000 property (like townhomes in Davenport or homes in Saint Cloud) requires a down payment of $70,000 at 25%. With closing costs and reserves, the total is around $90,000–$100,000. That’s significantly less than the $130,000–$150,000 of a $400,000 property.

The absolute dollar return is lower, but the percentage return can be similar, and the entry barrier is more accessible. A smaller first property that generates real cash flow or appreciation is better than an ideal property that never gets bought for lack of capital.

Among the new homes available in Saint Cloud from $333,000 there are options with 2025 delivery in new communities with good amenities that fit this first-investment profile with a lower entry threshold.

Strategy 5: accelerate savings with specific adjustments

There are concrete decisions that accelerate savings without requiring a radical lifestyle change. The goal is to increase the savings rate by 20%–30% during a defined period (2–3 years).

Audit fixed expenses. On average, an upper-middle-class Latin American family has between 3 and 6 subscriptions or services they pay for and rarely use. Every $100 per month freed up is $1,200 per year and $3,600 over three years.

Convert variable income into automatic savings. Bonuses, commissions, extraordinary fees. If every variable income goes directly to the dollarized account instead of merging into current spending, savings accelerate without feeling it.

Generate additional dollar income. International consulting, freelance work for U.S. or European clients, selling digital products. An additional income of $500–$1,000 monthly in dollars can cut the time to the down payment in half.

Use the yield on savings. If the $50,000 you’ve already saved is sitting in a zero-yield account, putting it in an American treasury bond fund at 4.5% annually generates $2,250 in a year, or $4,500 in two. Not a transformation, but not negligible either.

The realistic timeline from different starting points

| Current capital | Monthly savings | Estimated time to $140,000 |

|---|---|---|

| $0 | $3,000/month | ~4 years |

| $0 | $5,000/month | ~2.5 years |

| $30,000 | $3,000/month | ~3 years |

| $30,000 | $5,000/month | ~1.8 years |

| $70,000 | $3,000/month | ~2 years |

| $70,000 | $5,000/month | ~1.2 years |

These numbers assume savings are dollarized and that there’s no additional yield. With 4%–5% annual yield on accumulated savings, timelines are reduced by an additional 3 to 6 months.

Frequently asked questions

Can the down payment come from a loan in my home country?

Yes, in principle. But the American lender may ask you to document the origin of the funds. A loan in your country is documentable, but it also increases your total debt, which can affect the American loan analysis.

Can I use a 401k or a Latin American pension fund for the down payment?

In the U.S., there are penalties for withdrawing 401k funds before age 59.5 (10% penalty plus tax). For Latin American pension funds, it depends on each country’s legislation. In Colombia, for example, there are specific conditions under which pension funds can be accessed for home purchases.

Is it possible to get a bridge loan for the down payment?

Some American lenders accept “gift funds” as part of the down payment, as long as it’s documented as a gift and not a loan. A loan for the down payment is generally not accepted because it increases total leverage.

What if the exchange rate rises just before I need the money?

It’s a real risk for those saving in local currency. The solution is to dollarize savings as soon as possible to eliminate that timing risk. The longer savings are held in dollars, the less exchange rate exposure.

Is it worth waiting to have 30% down to get better terms?

In some cases, a 30% down payment can get you a rate 0.25%–0.5% lower on the loan, translating to $50–$100 less per month. If reaching 30% requires 12 additional months of saving, those 12 months without the asset generating income may cost more than the rate savings. The specific analysis depends on each case’s numbers.

If you want to calculate exactly how much you need for a specific property in Florida and build a realistic savings plan, our team can work through it with you. Use our free budget calculator and in one consultation we’ll put together the exact number and the shortest path to get there.