There’s one number that appears in every Florida real estate listing: the purchase price. What doesn’t appear is what it costs to maintain that property after you close. And that difference, for many Latin American investors, is what separates a profitable investment from one that drains money every month.

This article isn’t meant to discourage you. It’s to make sure you arrive at negotiations with the right numbers, because the real return on a property in Florida isn’t calculated on the sale price but on the total cost of ownership.

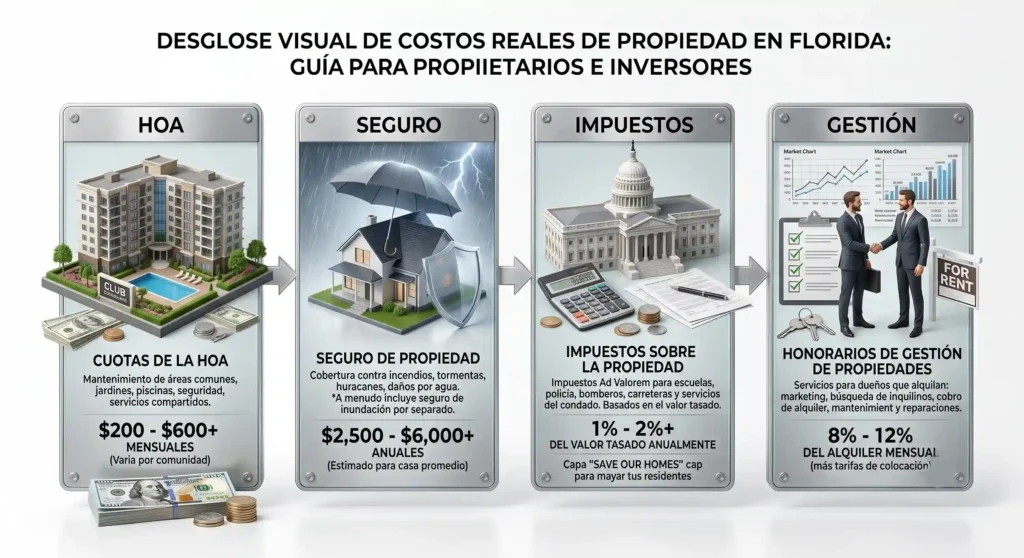

The costs you know (and the ones you probably underestimate)

When a Latin American investor calculates whether they can buy in Florida, they generally consider the property price and the down payment. Sometimes they add closing costs. Very few calculate the annual cost of keeping that property operating.

The difference between both calculations can be $15,000 to $30,000 per year depending on property type and location. Ignoring that doesn’t change the numbers — it just delays the surprise.

HOA: the cost that varies most and confuses most

The HOA (Homeowners Association) is the monthly fee paid to the community association. It covers maintenance of common areas, amenities, and shared services. In most gated communities around Orlando and Miami, it’s mandatory.

The range is wide. In basic residential communities, HOA can be $100 to $200 per month. In resort communities like Champions Gate or Reunion, where there are pools, water parks, courts, and concierge services, HOA runs between $400 and $700 per month. In luxury buildings in Brickell or Miami Beach, it can exceed $1,500 monthly.

What the HOA covers also varies. Some communities include building insurance, cable, internet, or lawn maintenance. Others cover only amenity access. Before buying, read the HOA budget document and review whether it has accumulated reserves. An HOA with low reserves can apply special assessments — extraordinary charges to cover major repairs.

| Community type | Estimated monthly HOA | What it typically includes |

|---|---|---|

| Basic townhome | $100–$200 | Exterior maintenance, common areas |

| Resort community (Kissimmee) | $400–$700 | Amenities, security, maintenance |

| Luxury building (Miami) | $800–$2,000+ | Insurance, concierge, premium amenities |

| Single family without HOA | $0 | Nothing (more control, more responsibility) |

Property insurance: the cost that has risen most in Florida

Property insurance in Florida has seen sustained increases since 2021. Several factors explain this: hurricanes, inflation in construction costs, and several insurers exiting the state market. In 2026, the average cost of home insurance in Florida is among the highest in the country.

For a $400,000 home in the Orlando area, insurance can cost between $3,000 and $6,000 per year depending on the property’s age, building materials, and distance from flood zones. For properties closer to the coast or in flood-risk zones, a separate flood insurance policy must be added, which can contribute an additional $1,500 to $4,000 annually.

Properties built after 2002, when Florida updated its building code following Hurricane Andrew, have better rates than older construction. Roof type, hurricane-protection windows, and the electrical system also factor in.

For vacation rental properties, some standard insurance policies don’t cover damage caused by tenants or guests from platforms like Airbnb. A specific short-term rental insurance policy is required, at an additional cost of $500 to $1,500 per year. A vacation rental insurance policy designed for foreign investors is the right coverage for this profile.

Property tax: how to calculate it correctly

Property tax in Florida is calculated on the assessed value of the property by the county office. The effective rate varies by county, but in the Orlando area (Orange and Osceola counties) it ranges between 0.8% and 1.2% of the assessed value annually.

For a $400,000 property, that represents between $3,200 and $4,800 annually.

There’s a detail many investors don’t know: the Homestead Exemption. If the property is your primary residence and you have Florida residency, you can apply for an exemption of up to $50,000 on the assessed value, reducing the tax. But non-resident investors using the property as a rental don’t qualify for this exemption.

Another relevant point: the assessed value can rise each year, which increases the tax. Florida limits the annual increase in assessed value to 3% for primary residences (Save Our Homes), but that limit doesn’t apply to investment properties.

| County | Estimated effective rate | Annual property tax ($400k property) |

|---|---|---|

| Orange (Orlando) | 0.9–1.1% | $3,600–$4,400 |

| Osceola (Kissimmee) | 0.8–1.0% | $3,200–$4,000 |

| Miami-Dade | 0.9–1.2% | $3,600–$4,800 |

| Broward (Fort Lauderdale) | 1.0–1.2% | $4,000–$4,800 |

Maintenance and repairs: the cost most underestimated

The general rule in American real estate investment is to reserve between 1% and 2% of the property value per year for maintenance and repairs. For a $400,000 property, that’s between $4,000 and $8,000 annually.

That figure seems conservative until the air conditioning system fails in July. In Florida, the HVAC (heating, ventilation and air conditioning) runs almost year-round. A full replacement costs between $5,000 and $12,000. The roof has a lifespan of 15 to 25 years depending on material; replacing it costs between $8,000 and $20,000.

For vacation rental properties, wear is greater because there’s constant guest turnover. Furniture, appliances, and finishes get used more intensively. The maintenance reserve remains necessary regardless of insurance coverage.

Property management: how much it costs to delegate operations

If you don’t live in Florida, you need someone to manage the property for you. The options are hiring a property management company or doing it remotely, which in practice is difficult to sustain well.

For long-term rentals, property management companies charge between 8% and 12% of the monthly rental income. For a property generating $2,000 per month, that’s between $160 and $240 monthly, plus possible additional fees for leasing, inspections, or coordinated repairs.

For short-term vacation rental, the model is different. Companies charge between 20% and 35% of the property’s gross income. In exchange, they handle the listing, guest communication, cleaning, and operational maintenance. For an investor thousands of miles away, that commission is usually worth what it costs.

The real total cost: an example with numbers

Take a home in Kissimmee priced at $420,000, financed with a 30% down payment ($126,000) and a loan of $294,000 at 8% over 30 years.

| Item | Monthly cost | Annual cost |

|---|---|---|

| Mortgage payment | $2,158 | $25,896 |

| HOA (resort community) | $500 | $6,000 |

| Property insurance | $375 | $4,500 |

| Property tax | $350 | $4,200 |

| Estimated maintenance (1.5%) | $525 | $6,300 |

| Property management (25% vacation rental) | $625* | $7,500* |

| Total costs | $4,533 | $54,396 |

*Estimated on $2,500/month gross vacation rental income.

For this property to be profitable, you need to generate more than $54,396 per year in rental income. With 70% occupancy and an average rate of $200/night, that’s achievable — but there’s no margin for error if occupancy drops or an extraordinary maintenance expense comes up.

The point isn’t that the investment is bad. It’s that the right decisions are made with these numbers on the table, not just the purchase price.

Frequently asked questions

Can the HOA be negotiated or is it fixed?

The HOA is not negotiable. It’s set by the homeowners association and applies equally to all owners. What you can evaluate before buying is the HOA’s history of increases and the state of its reserves.

Does home insurance cover hurricane damage?

Most standard policies in Florida include wind coverage, which covers hurricane damage. What it doesn’t cover is flooding. For that you need a separate flood insurance policy, especially if the property is in a FEMA zone.

How do I know if a property is in a flood zone?

You can check on the official FEMA map (flood.maps.fema.gov) using the property’s address. Your real estate agent is also required to disclose if the property is in a risk zone before closing.

Are maintenance expenses tax deductible?

Yes. If the property generates rental income, most operating expenses are deductible from taxable income in the U.S.: HOA, insurance, property tax, repairs, property management, and asset depreciation. An accountant specializing in real estate investments for foreigners can structure this correctly.

What happens if the HOA runs out of funds?

If the HOA can’t cover major repairs, it can issue a special assessment — an extraordinary charge to all owners. The amount can be hundreds or thousands of dollars. Before buying, review the HOA’s financial statements and ask if there are pending or projected assessments.

Are there properties in Florida without an HOA?

Yes, single-family homes outside gated communities exist without HOAs. They offer more freedom (you can rent without platform restrictions, for example), but also more direct responsibility for exterior maintenance and security.

Before closing any purchase, the most useful step is to review these numbers with someone who knows the specific market where you want to invest.

Request your free ROI analysis with our team