Insurance is the aspect of real estate investment that gets ignored most until something goes wrong. And when something goes wrong with a vacation rental property in Florida, the cost can be devastating: a guest injured at the pool, a hurricane that destroys the roof, a kitchen fire, a tenant who intentionally damages the property.

The question is not whether you need insurance. It is what type of insurance you actually need and how much it costs.

Why standard homeowner’s insurance does not work for a vacation rental

The most common mistake among property owners who first enter the vacation rental market in Florida is assuming that standard homeowner’s insurance (HO-3) covers their operation. It does not.

Standard HO-3 policies are designed for a primary or secondary residence used personally. When the property is used commercially to generate rental income, most insurers consider coverage void or limited for events related to that commercial use.

If an Airbnb guest falls by the pool and sues the owner, a standard HO-3 policy can deny coverage arguing the property was in commercial use. The result can be a liability lawsuit the owner faces without insurance backing.

The types of insurance a vacation rental property in Florida needs

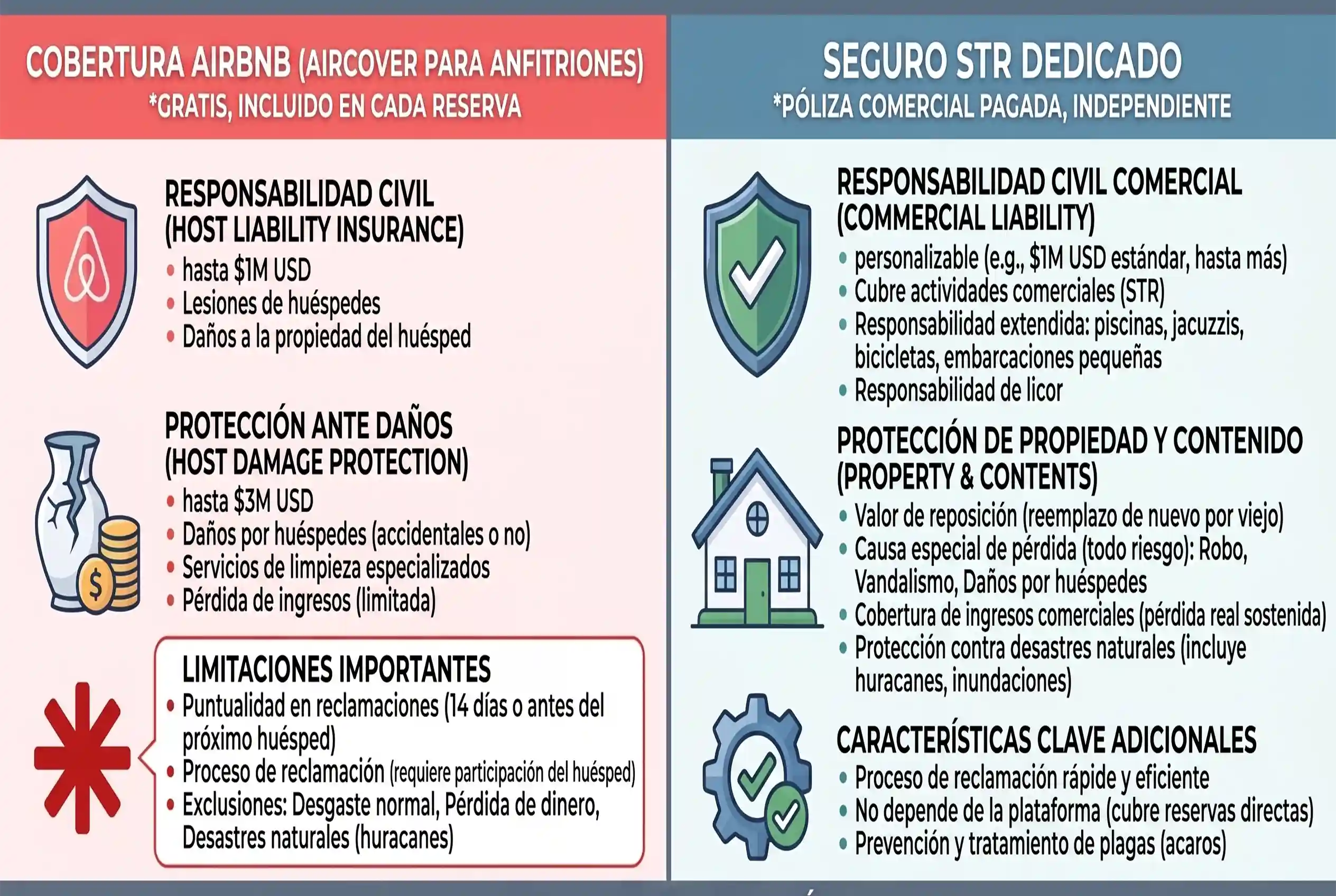

Short-Term Rental Insurance (STR Insurance) This is the specific policy designed for vacation rental properties. It covers civil liability toward guests, structural damage caused by tenants, loss of income from damage that makes the property uninhabitable and in some cases, intentional damage caused by guests.

Insurers that offer specific STR policies include Proper Insurance, Slice Insurance and some specialized programs from larger insurers. Premiums vary widely based on zone, property value and coverage selected.

Flood insurance Mandatory if the property is in a FEMA-designated flood zone and has a mortgage. Highly recommended in any case in Florida given the hurricane history. Standard homeowner’s policy does not cover flooding — they are separate products.

Flood insurance is obtained through the National Flood Insurance Program (NFIP) or private insurers. In high-risk zones like parts of Cape Coral or Miami coastal properties, the cost can exceed $5,000 annually.

Wind and hurricane insurance In Florida, many standard policies exclude wind damage or cover it with very high hurricane-specific deductibles (generally 2% or 5% of the insured value, not a fixed amount). For a $400,000 property, a 5% hurricane deductible is $20,000.

In coastal or higher wind-risk zones, wind insurance can be purchased separately through Citizens Property Insurance Corporation, Florida’s insurer of last resort.

You can review how these considerations affect the analysis of a specific investment in our vacation home ROI in Orlando analysis.

Coverage comparison table for vacation rentals in Florida

| Policy type | Covers liability | Covers guest damage | Covers flooding | Covers wind/hurricane | Annual reference cost |

| Standard HO-3 | Partially (personal use) | No | No | Varies | $1,500 – $3,500 |

| STR Insurance (Proper, Slice) | Yes, commercial use | Yes | No (separate) | Varies | $2,500 – $6,000 |

| NFIP (federal flood) | No | No | Yes | No | $800 – $5,000+ |

| Citizens / wind insurance | No | No | No | Yes | $1,200 – $4,000 |

| Airbnb AirCover | Limited | Yes (up to $3M) | No | No | Included in platform |

Costs are reference data for a $400,000 to $500,000 property in central Florida. Coastal zones have significantly higher premiums.

What Airbnb covers and what it does not

Airbnb offers hosts AirCover, which includes civil liability protection up to $1 million and coverage for damage caused by guests. In 2023 they expanded damage coverage to $3 million in some cases.

What AirCover does not cover: structural hurricane damage, flooding, fire unrelated to guests, damage to vehicles on the property, high-value valuables and loss of income from causes unrelated to guest damage.

Airbnb coverage is a supplement, not a replacement. Using it as your only protection is a mistake that can be very costly if a major event occurs.

What full insurance actually costs for a vacation property

For a $450,000 vacation home with pool in Kissimmee or Davenport, reasonable complete coverage includes:

- STR policy: $3,500 – $5,000 annually

- Flood insurance (if FEMA zone applies): $1,200 – $2,500 annually

- Additional wind coverage (if not included in STR): $1,000 – $2,000 annually

- Estimated total: $4,500 – $9,500 annually

That range seems wide because it is. The difference between $4,500 and $9,500 depends on the specific zone, claims history, construction type and insurer.

What is clear is that insurance must be included in ROI calculations from the start. An investor who calculates profitability with $2,000 in insurance when the actual premium is $6,500 is working with fictional numbers.

To review how insurance and other fixed costs affect the real return of a property before buying, the Florida HomeGroup Realty team can build a realistic financial projection for you.

FAQ about vacation rental insurance in Florida

Can I get STR insurance as a foreign owner without US residency?

Yes. Most insurers offering STR policies in Florida do not require the owner to be an American resident. You will need an ITIN or EIN, property manager information and the property address details. Some insurers work directly with property managers to facilitate the process.

Does insurance cover if a guest cancels due to a hurricane?

Not directly. Platforms like Airbnb have force majeure cancellation policies that may generate guest refunds. Some STR policies include loss of income coverage if the property becomes uninhabitable due to covered damage, but they do not cover preventive cancellations.

Do I need to declare to my insurer that the property is rented on Airbnb?

Yes. Not declaring it can void the entire policy. Property use is material information for the insurer. If you have an HO-3 policy and start renting without notifying them, you may be without coverage precisely when you need it most.

Does the community insurance (master policy) cover my unit?

In condominiums and some gated communities, there is a master policy that covers the exterior structure and common areas. That policy does not cover the interior of your unit or your civil liability as a host. You need an additional individual policy.

Insurance is not the most exciting aspect of a real estate investment. It is also not optional if you want the investment to survive an unexpected event. Calculating ROI without including the real cost of insurance is like calculating the fuel for a trip without counting tolls.

Request your profitability analysis by zone with real insurance costs included