Why this loan works differently from everything else

When a foreign investor wants to buy a property in Florida, the conversation almost always ends the same way: you need credit history here, an American tax return, verifiable U.S. employment. For conventional mortgages, that’s true. For the DSCR loan, none of it applies.

The DSCR doesn’t analyze your income. It analyzes the property’s income. If the house generates enough rent to pay its own loan, you qualify. That’s it.

That opens a door most Latin American investors didn’t know existed. This guide covers how the calculation works, which lenders work with non-residents, how much you need as a down payment, and a real-number example with a $350,000 property in Orlando. If you’re still deciding whether Florida is the right market before diving into financing, this guide to investing in Orlando real estate as a foreigner gives you the market context first.

How the DSCR works

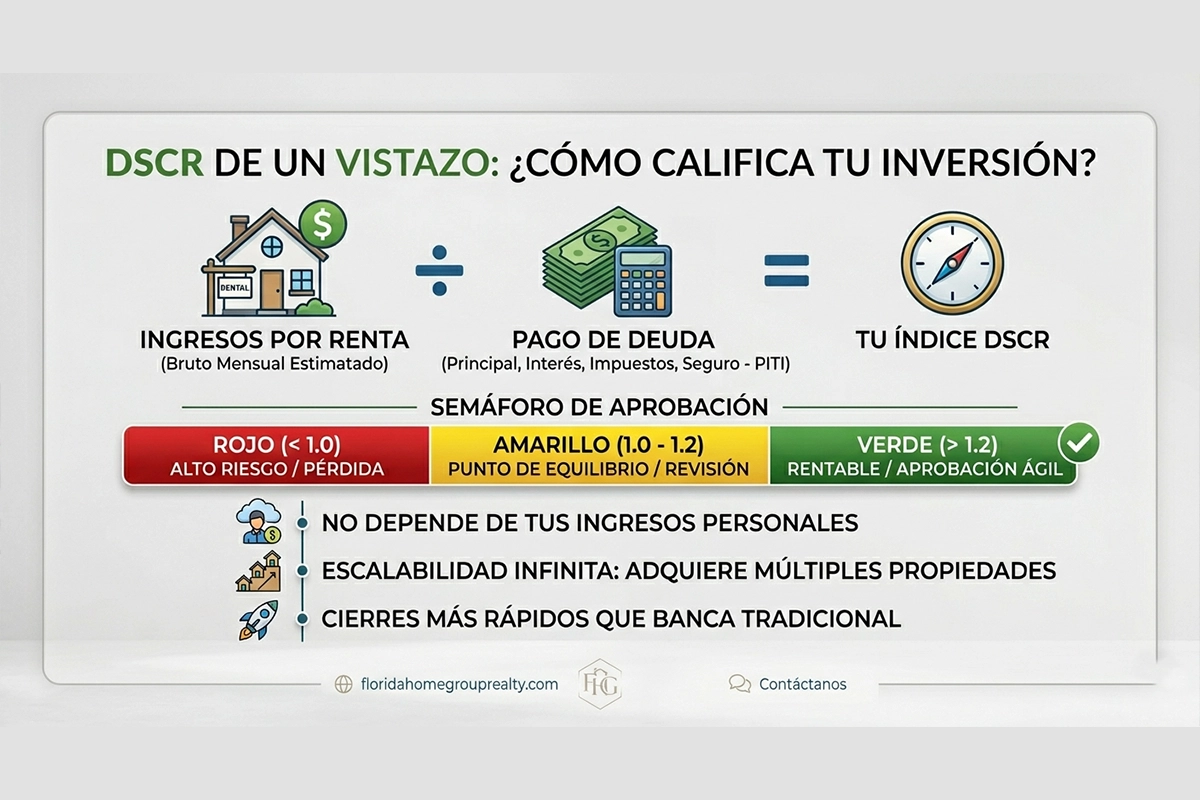

DSCR stands for Debt Service Coverage Ratio. What it measures is straightforward: does this property generate enough rent to cover its own loan?

Formula: DSCR = Gross monthly rent ÷ PITIA (Principal + Interest + Taxes + Insurance + HOA if applicable)

Concrete example: a property with $2,800 in monthly rent and a PITIA of $2,150 produces a DSCR of 1.30x. Most lenders require at least 1.20x to 1.25x to approve.

What if the ratio falls below 1.0x? The property doesn’t cover its own loan. Some lenders work with lower ratios, but they charge more and require a larger down payment. Not the best starting point.

What if the property is vacant? The lender requests a rent appraisal — a licensed appraiser certifies what the property would generate in the current market. If you already have a signed lease, that works too.

The numbers: $350,000 property in Orlando

Here’s how a DSCR lender would run the numbers in 2026:

| Concept | Value | Detail |

| Purchase price | $350,000 | Orlando, FL |

| Down payment (25%) | $87,500 | Initial capital |

| Loan amount | $262,500 | 75% financed |

| Monthly rent | $2,800 | Estimated income |

| Monthly PITIA | $2,150 | Principal + Interest + Taxes + Insurance |

| Resulting DSCR | 1.30x ✓ Approved | 2,800 / 2,150 = 1.30 |

With that ratio, the investor qualifies without presenting a U.S. tax return or employment letter.

What types of lenders work with foreigners

Not everyone who advertises DSCR loans works with clients who have no U.S. residency. Here’s what to expect from each type in 2026:

| Type | Min. DSCR | Down payment | Est. rate | Closing | Note |

| Regional banks | 1.25x | 25% | 7.5%–8.5% | 45–60 days | May require U.S. history |

| Mortgage brokers | 1.20x | 20–25% | 7.0%–8.0% | 30–45 days | More flexible with foreigners |

| Private lenders | 1.10x | 30% | 8.5%–10% | 15–30 days | Fast but most expensive |

| Credit unions | 1.25x | 20% | 6.8%–7.8% | 45–60 days | Require membership |

Rates change based on market conditions and investor profile. Request formal pre-qualification before comparing.

Documents you’ll need

From the investor:

- Valid passport (visa if applicable)

- ITIN or EIN if operating through an LLC

- Bank statements from the last 2–3 months showing funds for down payment and reserves

- International credit history, or FICO 620+ if you have U.S. credit history

From the property:

- Signed purchase contract

- Rent appraisal certified by a Florida-licensed appraiser

- Property inspection

- Property insurance before closing

Standard conditions:

- Down payment: 20%–30% of purchase price

- Minimum DSCR: 1.20x

- Reserves: 6–12 months of PITIA in a verifiable account

- Property: residential 1–4 units, condominiums, or STR with specific approval

What properties qualify

Qualify: single-family homes (most lenders, most straightforward process), duplexes, triplexes, fourplexes, condominiums (with project restrictions), townhouses, and vacation rentals (Airbnb / STR) with a specialized lender.

Don’t qualify: commercial properties, undeveloped land, and buildings with more than 4 units. Those require commercial financing with a different structure.

The advantages are real. So are the costs.

The DSCR solves the central problem of the foreign investor: no U.S. income or credit history required, the process is faster than a conventional mortgage, and you can structure it under an LLC.

But the numbers need to be clear: rates run 0.5% to 1.5% higher than conventional loans, the minimum down payment is 20%–30%, and the reserves lenders require are usually more than most people expect. It’s not a cheap loan. It’s an accessible loan when the other doors are closed.

What makes it attractive:

- No verifiable U.S. income or employment required

- No W-2 or American tax return

- Faster process than a conventional mortgage

- Can be structured under an LLC

- Scales your portfolio without your personal debt-to-income ratio blocking you

What you need to understand going in:

- Rates 0.5%–1.5% higher than conventional mortgages

- Down payment of 20%–30% — not the 3–5% available to residents

- More demanding bank reserve requirements than most expect

- Not available for primary residence

- Some zones and property types don’t qualify

For investors who already have a property and want to use their accumulated equity to fund the next purchase, this guide on refinancing in Florida as a foreigner covers how the DSCR cash-out refi works and when it makes sense to use it.

FAQ

What is the DSCR?

The relationship between what the property generates in rent and what the monthly loan costs. A ratio of 1.25x means it produces 25% more than it needs to service its debt.

Do I need U.S. credit history?

Not necessarily. The DSCR evaluates the property’s cash flow. A FICO of 620+ improves the terms, but it’s not mandatory in all cases.

How much down payment do I need?

Between 20% and 25%. Below that threshold, some lenders require higher additional reserves.

Do I qualify as a foreigner without residency?

Yes. The DSCR exists precisely for that profile.

What properties are accepted?

Residential properties from 1 to 4 units, condominiums, townhouses, and vacation rentals with specific approval.

How long does the process take?

Between 15 and 60 days. Private lenders close faster but charge more; brokers are usually the middle ground on price and speed.

Ready to evaluate your first DSCR loan in Florida?

En Florida HomeGroup Realty conectamos a inversores extranjeros con los lenders DSCR adecuados para su perfil. Sin costo, sin compromiso.