Why fast financing exists — and when you need it

A hard money loan doesn’t compete with a DSCR loan. They’re tools for different moments. The DSCR is for acquiring and holding stabilized properties. The hard money is for opportunities that can’t wait 30 days — a foreclosure, an off-market deal with an urgent closing deadline, or a property that needs so much renovation that no conventional bank will touch it.

The price of that speed is the rate: a hard money loan in Florida in 2026 costs between 10% and 14% annually plus origination points. It’s not cheap. But if the deal has the right margin, the cost of financing is just another line in the analysis — not the factor that determines it.

For foreign investors, hard money has an additional advantage: many lenders don’t require American income or U.S. credit history. The collateral is the property. If the deal is solid, the loan flows. If you’re still figuring out how to structure your entry into the market, this guide to financing options for investing in Florida gives you the full picture before choosing a product.

How a hard money loan works in Florida

The logic is simple: the lender lends based on the asset’s value, not your credit profile. Typical parameters in the Orlando 2026 market:

| Parameter | Typical range Florida 2026 |

| LTV (on purchase price) | 65–75% of purchase price |

| LTC (loan to cost, purchase + rehab) | 80–90% of total deal cost |

| ARV (on post-renovation value) | Up to 70% of ARV |

| Interest rate | 10–14% annually (interest-only during the term) |

| Origination points | 2–4 points (% of loan amount) |

| Loan term | 6–24 months |

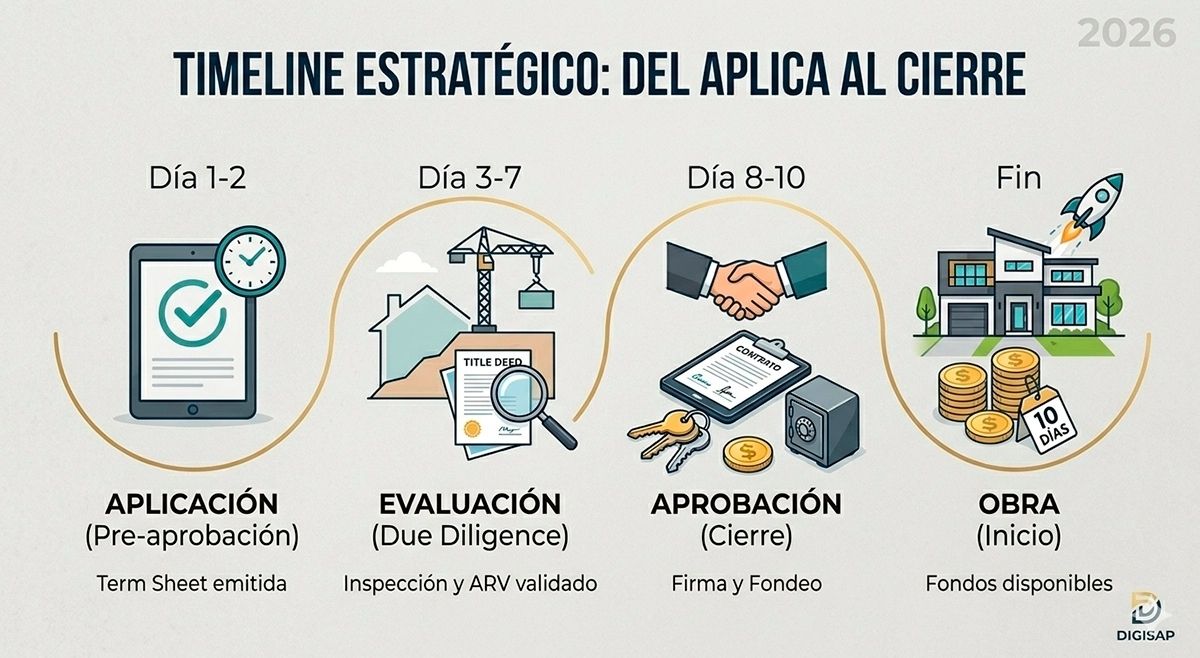

| Closing speed | 7–14 days from approved application |

| U.S. income required | No for most lenders — collateral is the asset |

| U.S. credit history | Flexible — some lenders accept without American score |

Full numerical example: flip $200K to $310K in Orlando

You bought a distressed house in a developing neighborhood in East Orlando for $200,000. The ARV (after repair value) based on comparables is $310,000. The renovation budget is $45,000.

| Concept | Amount |

| Purchase price | $200,000 |

| Hard money loan (70% LTV) | $140,000 |

| Your down payment | $60,000 |

| Renovation cost | $45,000 |

| Origination points (3 points on $140K) | $4,200 |

| Holding interest 6 months (12% annual) | $8,400 |

| Closing costs (purchase + sale) | $12,000 |

| Total deal cost | $269,600 |

| Sale price (ARV) | $310,000 |

| Gross profit before taxes | $40,400 |

| ROI on own capital ($60K + extras) | ~126% on invested capital |

Note for foreign investors: FIRPTA withholds 15% of the gross sale price at closing ($46,500 in this case). It’s recoverable through your tax return, but it affects your immediate cash flow. Plan with a CPA before executing the flip. To understand exactly how this mechanism works and what other taxes apply on a sale, this guide to taxes when selling a property in Florida covers the process with real numbers.

Hard money vs DSCR vs conventional loan — when to use each

| Factor | Hard money | DSCR loan | Conventional |

| Closing speed | 7–14 days | 21–35 days | 30–45 days |

| Typical rate | 10–14% annual | 7–8.5% annual | 6.5–7.5% annual |

| Damaged / fixer property | Yes — this is the product for it | No — must be habitable | No — requires clean appraisal |

| U.S. income required | No for most | No — qualifies by rent | Yes — W-2 or tax returns |

| Maximum term | 6–24 months | 30 years | 15–30 years |

| Total financing cost | High — ideal for short deal | Moderate — for hold | Low — for long-term hold |

| Typical use | Fix & flip, BRRRR step 1, bridge | Buy and hold, BRRRR refi | Residents with U.S. income |

Hard money as a bridge — most common use cases

- Fix and flip: you buy a distressed property, renovate it, and sell before the hard money term expires

- BRRRR step 1: you use hard money to buy and renovate, then refinance to DSCR once the property is stabilized and rented

- Bridge loan: you need to close a purchase fast before your current property sells or before a conventional DSCR processes

- Foreclosure or auction property: auction processes require fast closing — hard money is often the only viable option

Documents you need for a hard money loan as a foreigner

| Document | Detail |

| Valid passport | Primary identification for the lender |

| Proof of funds | Bank statement from the last 3 months showing the down payment |

| Scope of work | Detailed renovation budget with contractor or estimates |

| Comparables (ARV) | CMA or appraisal supporting the projected post-renovation value |

| Purchase contract | Signed purchase agreement by both parties |

| Entity docs (if applicable) | Florida LLC articles of organization if buying under an entity |

Risks of hard money you need to know before using it

- Term expires before renovation is complete: if the rehab runs long and the loan matures, the lender can foreclose — always negotiate extensions from the start

- ARV doesn’t hold: if the market drops or comparables don’t support the projected value, the deal’s margin disappears

- Renovation costs exceed budget: every dollar of overrun comes out of your margin — hard money doesn’t cover surprises

- Can’t get the DSCR refi post-renovation: if the plan is BRRRR and the DSCR lender doesn’t approve, you’re left with the hard money running — identify your exit lender before you enter

FAQ

What is a hard money loan in simple terms?

A short-term loan (6–24 months) secured by the property, not by your income or credit history. The lender moves fast (7–14 days) at higher rates (10–14%) because they assume more risk and lend on properties conventional banks reject. It’s speed financing, not long-term financing.

Can a foreigner get a hard money loan in Florida?

Yes. Most hard money lenders in Florida work with foreign investors — the collateral is the property, not your profile in the American financial system. You need a passport, proof of funds for the down payment, and a deal with numbers that support the loan.

What does a hard money loan really cost?

In the example of $140,000 borrowed at 12% annually for 6 months with 3 origination points: $8,400 in interest + $4,200 in points = $12,600 total financing cost. It’s significant — that’s why hard money deals need margins of at least 20–25% over total cost to be viable.

How long does a hard money loan take to close?

Between 7 and 14 days from when the lender approves the deal and scope of work. That’s the main advantage over any other financing product. Some specialized lenders close in 5 days on clean deals. Compared to 30–45 days at a conventional bank, the difference can be decisive for winning a competitive deal.

Did you find a deal that can’t wait 30 days?

Visit our contact page or message us on WhatsApp and receive personalized advice based on your investment profile.