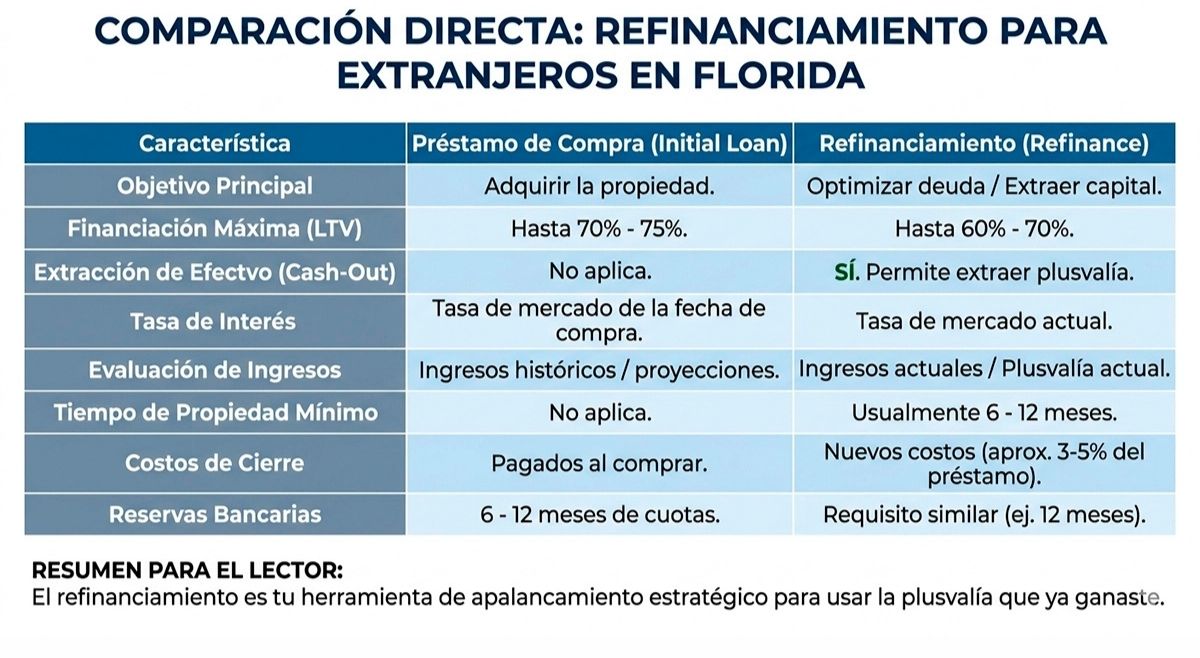

Why refinancing exists — and why most investors ignore it too long

When you buy your first property in Florida, the focus is on closing. Then comes management, tenants, cash flow. Refinancing gets pushed to later.

That “later” is where portfolios get built. The property you bought for $300,000 is worth $400,000 today. You have $150,000 in equity sitting there doing nothing. A cash-out refinance converts that equity into liquidity to buy the next property — without selling the one you already have.

The problem for foreign investors is that not all lenders refinance without a U.S. W-2. But the ones that do — especially those working with DSCR products — are enough to build a solid portfolio. If you’re at that growth stage, this guide on how to build a real estate portfolio in Florida gives you the complete framework for scaling with strategy.

The three types of refinancing you need to know

-

Cash-out refinance

You replace your current mortgage with a new, larger loan and pocket the difference in cash. It’s the most direct way to extract equity without selling the property.

-

Rate-and-term refinance

You change the rate, the term, or both — without pulling out cash. Useful if rates dropped since your original purchase, or if you want to move from a 15-year to a 30-year loan to reduce the monthly payment and improve cash flow.

-

DSCR refinance

Refinancing with a DSCR product means the lender qualifies the property based on its rental income, not your personal income. For foreigners, it’s the most accessible path. It works for both cash-out and rate-and-term.

Refinancing types compared

| Refi type | Min. equity | Est. rate | Documents | Ideal for |

| Cash-out (DSCR) | 25–30% | 7.5–8.5% | Passport + property rent | Extracting capital for next purchase |

| Rate-and-term (DSCR) | 20% | 7.0–8.0% | Passport + property rent | Lower payment, improve cash flow |

| Conventional cash-out | 20% | 6.5–7.5% | W-2 + U.S. tax history | Residents with documented U.S. income |

| HELOC | 15–20% | Variable (prime+) | W-2 generally required | Flexible credit line (difficult for foreigners) |

Note: For most foreign investors, the DSCR refinance — whether cash-out or rate-and-term — is the only practical path without U.S. income documentation.

Real example: $400,000 property with $150,000 in equity

You bought a house in Orlando for $300,000 three years ago. Today the market value is $400,000 and your mortgage balance is $250,000. That gives you $150,000 in equity — 37.5% of the current value.

| Concept | Amount |

| Current property value | $400,000 |

| Current mortgage balance | $250,000 |

| Available equity | $150,000 |

| New loan (75% LTV of value) | $300,000 |

| Previous mortgage payoff | -$250,000 |

| Closing costs (est.) | -$8,000 |

| Net cash you receive | ~$42,000 |

| New monthly payment (7.5%, 30 years) | ~$2,097 |

| Property rental income | $2,800/month |

| Net cash flow (post-refi) | ~$703/month positive |

Result: you have $42,000 in cash to use as a down payment on the next property, and the first one keeps generating positive cash flow. That’s equity working.

What you need to refinance as a foreigner in Florida

| Requirement | Detail |

| Minimum equity | 20–30% of current property value (LTV 70–80%) |

| Ownership time | Generally 6–12 months from purchase (seasoning period) |

| U.S. income required | No for DSCR products — the property’s rent qualifies |

| Credit score | 680+ preferred; international credit history accepted with some lenders |

| Required documents | Valid passport, bank statements (3 months), lease agreement or rent analysis |

| ITIN accepted | Yes with most DSCR lenders — verify before applying |

| LLC accepted | Yes — many DSCR lenders allow refi under an entity |

| Required reserves | 3–6 months of PITIA in liquid assets post-closing |

Step by step: how to refinance

- Verify your current equity. Request a market value assessment — your agent can run a comparative market analysis (CMA) at no cost.

- Calculate your target LTV. If your property is worth $400K and you want a cash-out at 75% LTV, your new loan will be $300K.

- Contact DSCR lenders specialized in foreigners. Not all refinancing lenders work with non-residents — filter from the start.

- Get an updated rent analysis. The lender needs to confirm that the current rental income covers the new payment (DSCR above 1.0).

- Gather your documents: passport, bank statements, active lease agreement or property management letter.

- Open or confirm your U.S. bank account. The cash-out funds get deposited there. If you don’t have one yet, this guide on how to open a bank account in the U.S. as a foreigner covers the process before you start.

- Close the refinance. Takes between 21 and 45 days from application. Funds arrive 3 business days after closing.

When refinancing makes sense — and when it doesn’t

| Refinancing DOES make sense if… | Refinancing DOESN’T make sense if… |

| Your equity exceeds 30% and you have a clear plan for the cash | You don’t have a property or clear strategy for investing the cash-out |

| The new rate improves your monthly cash flow | The new rate is equal or higher and you’re not extracting cash |

| You’ll use the cash as a down payment on the next purchase | You’ll use the cash for consumer expenses unrelated to investment |

| Your property has a tenant with an active lease | The property is vacant — the lender can’t calculate the DSCR |

| At least 6–12 months have passed since purchase (seasoning OK) | You bought less than 6 months ago — most lenders require seasoning |

FAQ

Can I refinance a property in Florida as a foreigner?

Yes. With a DSCR product the lender qualifies using the property’s rental income, not your personal income. You don’t need a W-2 or American tax history. The main condition is having enough equity — generally 20–30% of the current value.

How much equity do I need for a cash-out refinance?

Most DSCR lenders lend up to 75–80% of the property’s value (LTV). If your house is worth $400,000, the maximum new loan would be $300,000–$320,000. Your equity after the refinance must be at least 20%.

How long do I have to wait to refinance after buying?

Most DSCR lenders require a seasoning period of 6 to 12 months from the purchase date. Some allow refinancing earlier if the property had significant documented appreciation, but those are the exception.

Does a cash-out refinance have tax implications for me as a foreigner?

The cash you receive from a cash-out is not income — it’s debt, so it doesn’t generate tax at the time of the refinance. However, the interest on the new mortgage may be deductible if the property generates rent. Consult a CPA specializing in foreign investments in the U.S. before closing.

What happens to my current rate if I refinance?

With a refinance, your current mortgage is paid off in full and replaced with the new loan. If your original rate was better than the current market rate, a cash-out refi raises your financing cost. Model the impact on monthly cash flow before deciding — it’s not always worth it even if you have a lot of equity.

Do you have equity in Florida and want to put it to work on your next property?

Visit our contact page or message us on WhatsApp and receive personalized advice based on your investment profile.